Sunday, December 09, 2007

Is this the way to go?

Generally its not good form to blog by just lifting in their entirety other peoples articles. But when you do, you are actually paying them a pretty big complement.

Such is the case with this very imformative article comparing the recent economic performance of Chile and Venezuela. Given that Chile has frequently been presented as a model that Venezuela should emulate this really is essential reading:

It would seem Chile is not all it has been cracked up to be.

The sad reality here is that neither of these countries are in very good shape. Venezuela is poor and very heavily dependent on one export commodity. And so far attempts to diversify the economy seen either not to exist or not to have had success.

Chile, contrary to popular perception, is also very dependent on export of a single commodity. And while it has had more success than Venezuela in increasing other exports those other exports seem also to be commodities or agricultural products. In other words, both countries are on the bottom of the world wide food chain exporting only natural resources and agricultural products - for some reason value added manufactures seem to be beyond them.

But one point is crystal clear. Chile, being to a large extent stuck in the same swamp of underdevelopment that Venezuela is, can hardly serve as a model for how Venezuela is to get out that underdeveloped state.

For that Venezuela would do MUCH better to look east towards South Korea and Tawain than to look south towards Chile.

|

Such is the case with this very imformative article comparing the recent economic performance of Chile and Venezuela. Given that Chile has frequently been presented as a model that Venezuela should emulate this really is essential reading:

Chile - Venezuela: The Hidden Weakness of a Strong Economy

By Mark Turner

Here is a quiz for you: Which South American nation:

a) depends on one single product for the majority of its exports?

b) derives 35% of its total GDP from said product?

c) has relied on the sharp rise in world market prices for its product to fuel growth?

d) has not added significantly to its international currency reserves in the period?

e) is often lauded as the LatAm model economy by world peers?

f) may possibly be worried about forward macro effects of the recent drop of over 20% in world market prices for its main product?

If you guessed Venezuela then began to doubt your choice, this analyst would not be at all surprised. The answer is Chile, and the major product in question is copper.

Most people with interest in hard commodities know that Chile is the world’s number one copper producing nation, and it is also owner of the world’s biggest copper producer in state-run Codelco. What most people do not realize is the growing dependence Chile has on commodity growth due to the rise in price of copper in this decade. Copper has always been central to Chile’s economy of course, but in recent times this dependence seems to have become a veritable addiction. While revisiting the Chilean macroeconomic situation recently, we were immediately struck by the similarity between the positions of Chile and Venezuela, and began to wonder why Venezuela was the recipient of such bad press for its virtual petroleum monoculture economy while the growing dependence Chile has on copper was all but ignored by otherwise astute economists.

Firstly, some basic parameters. With a population of 15 million, Chile has a little over half the citizens of Venezuela. Therefore when we see the 2006 GDP figures for Chile at U$205Bn and Venezuela at U$176Bn (both purchasing power parity figures from the respective central banks) and GDP per capita at around U$9000 for Chile and U$6100 for Venezuela, it makes sense that Chile is classed the “richer” of the two countries. The general perception is that growth in Chile is of the “steady and sustainable” type, which is based on exports, direct foreign investment and demand from a developed internal economy.

As the above chart shows, GDP growth has been fluctuating per quarter around this 5% level, but has been far below that of Venezuela. Venezuela’s well-publicized growth has come almost entirely from the rise in oil prices, of course. But Chile’s growth has been largely dependent on copper in the same period, as the following chart begins to demonstrate.

Since 2004, the export mix from Chile has changed substantially. Previously, copper made up between 35% and 40% of total exports by revenue, but this figure has ballooned to 60% in recent months. The correlation between this rise and the spot price of copper is fairly straightforward.

And as the next graph further illustrates, copper is the clear driving force behind the rise in export revenues.

According to central bank figures, Chile obtains 35% of GDP from copper and copper alone, revenue coming from the state run Codelco and from tax revenues from private mining companies. Taxes on mining are comparatively low in Chile, with the base rate set at 17%. Added to this is a 35% repatriation tax on earnings for foreign mining companies as well as royalty payments that range between 0.5% and 5% of gross revenues depending on amount of production per company, tax regime and spot commodity prices. However the state also offers significant tax breaks to foreign companies in the form of asset depreciation credits. In recent times, Chile has also tightened up tax loopholes that previously allowed foreign miners to avoid the full burdens via transfer pricing to parent companies abroad.

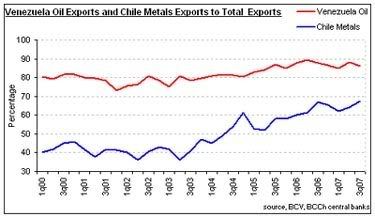

Coincidentally, according to the Banco Central de Venezuela (BCV), 35% of Venezuela’s GDP also comes via its main export, that of oil. In the case of Venezuela, around 80% of revenues come via its state-run oil company, PdVSA, with around 20% currently made by private (and mostly foreign) oil companies. In the next chart we see the total percentage of export revenues that come via oil in Venezuela and copper in Chile, and although Venezuela’s dependence is clearly stronger, copper in Chile is playing catch-up. To recap, 35% of Chile’s GDP and 67% of its exports currently come from copper. 35% of Venezuela’s GDP and 88% of its exports come from oil. But despite this, the perception is that Chile has a far more diversified economy.

Exports alone do not tell the full macro story, of course. We shall therefore take a look at some other macro indicators to measure the two countries. When it comes to inflation, Chile runs headline figures that beat Venezuela easily. Although Chile’s inflation rate has recently crept up from under 3% to the present 3.7%, it is still well below the Venezuelan rate that has fluctuated between 15% and 20% this year. However the following chart demonstrates that, surprisingly, the real world effects of inflation have been more severe in Chile than in Venezuela. The chart compares salary growth of the two nations with inflation via the consumer price indices. As we can see, Salaries have kept up with and in fact beaten the price rises in Venezuela, but in Chile’s case the reverse is true.

Venezuela has also made the best progress in combating unemployment. The next chart shows the seasonally unadjusted rates for both countries, and Venezuela has managed to cut unemployment in half since the dog days of the PdVSA strike in 2003. Chile has also made progress on this score, but the progress has been more moderate.

But on the subject of international reserves, there is no contest. Venezuela has managed to grow its safety cushion of international reserves significantly in this period, and even allowing for the U$5Bn withdrawn from the system by President Hugo Chávez in early 2007 to fund social programs, Venezuelan reserves have more than doubled since January 2003. On the other hand, Chilean reserves have stayed stubbornly at the same level in all this time, despite the boom in copper prices that has been every bit as impressive as oil prices. However, for whatever reason Chilean international reserves never seem to command the column inches of the Venezuelan figures. This analyst remembers the shock and gloom stories from publications a reputable as the London Financial Times in May 2007, bemoaning the drop in Venezuelan reserves to U$24Bn and predicting all sorts of problems in the near future. Since then reserves have risen to the current U$30Bn level, and the press has been strangely quiet on the subject. One wonders why.......

So which country is more prepared for any downturn in international commodities prices? The above figures seem to suggest that Venezuela is better placed than many imagine to ride out any forward weakness, but Chile’s more diversified economy should also be taken into account. Although Chile is obviously dependent on copper, it is worth noting that exports of other products have increased in the period in question. As the next chart shows, exports in absolute terms of non-metallic goods have risen in the course of this decade as Chile is also a major exporter of products such as fish, fish meal, fruits, wines etc. Chilean exporters though are fighting an uphill struggle against a perpetually rising currency.

Notwithstanding, the progress made by Venezuela in accumulation of international reserves far outstrips that of Chile, even though the more southerly nation runs a type of current account with the IMF that allows it to deposit and withdraw funds at any given moment in an attempt to allow smoother expenditure over the irregular period of income from commodities.

As for that future, recent price action suggests that Chile’s main export is looking weaker than that of Venezuela’s. LME spot copper has fallen over 20% in recent weeks, but the rise of oil on world markets to near U$100/bbl levels hardly needs much further comment here. Present copper weakness has been fuelled by the 18% YoY production rise inside China, with many analysts predicting that the world’s largest consumer will not be buying so much at the world market in 2008. ICSG figures currently point to world supply and demand at an equilibrium, which differs sharply from the supply constraints in petroleum products that come more from limited capacity growth in refineries more than the supply of crude from the ground or geopolitical pressures.

It should be stressed that direct employment in Chilean mining and Venezuelan oil makes up around 1% of the total workforce of each country, so the effects of a downturn would not show themselves in any layoff measures from either sector. However, in the same way that PdVSA is the main wealth producer in Venezuela, the copper mining industry in Chile plays the same role. In a 2006 survey by Ecoconsult, 92% of wealth creation in Chile was confined to Codelco and two other major copper miners.

Politically, Chile has been coming under greater pressure from its populace to spend more of its copper windfall. Polls suggest that two out of three Chileans want its government to relax the saving rules with the IMF and spend more of the windfall on social projects. This makes sense in a country that is ostensibly prosperous, but in fact runs the second highest level of social inequality in the LatAm region.

Conclusion

We chose Venezuela as the mirror to reflect on the state of play in today’s Chile for two main reasons, namely the dependence on one single export for the ongoing well-being in the countries and the vast difference in perception amongst other nations towards the countries. The administrations of both countries profess to be socialist, but the government of Hugo Chávez in Venezuela has, rightly or wrongly and for various reasons, a polemic position amongst fellow nations, with many seemingly desperate for the time that its president is toppled due to a sudden drop in oil prices. However the sound reputation and good standing of today’s Chile is to a very great extent also highly economically dependent on a single export, but for whatever reason it does not grab the limelight in the same way as Hugo’s black gold.

We therefore wonder how much the ‘A’ rating S&P has on Chilean sovereign bonds has to do with purely economic concerns and how much political stability seeps into the equation. We are sure the stability (or the lack thereof) will be front and center in both countries if the price of copper and oil take a sudden and drastic turn for the worse in the next few years.

Mark Turner is a cognitive scientist, linguist, and author.

It would seem Chile is not all it has been cracked up to be.

The sad reality here is that neither of these countries are in very good shape. Venezuela is poor and very heavily dependent on one export commodity. And so far attempts to diversify the economy seen either not to exist or not to have had success.

Chile, contrary to popular perception, is also very dependent on export of a single commodity. And while it has had more success than Venezuela in increasing other exports those other exports seem also to be commodities or agricultural products. In other words, both countries are on the bottom of the world wide food chain exporting only natural resources and agricultural products - for some reason value added manufactures seem to be beyond them.

But one point is crystal clear. Chile, being to a large extent stuck in the same swamp of underdevelopment that Venezuela is, can hardly serve as a model for how Venezuela is to get out that underdeveloped state.

For that Venezuela would do MUCH better to look east towards South Korea and Tawain than to look south towards Chile.

|

![]()